- How to Use AI in Content Marketing: Practical Use Cases, Tools & Best Practices - July 7, 2026

- The History of Stablecoins - May 1, 2026

- Why Money20/20 Europe 2026 Feels Different - March 27, 2026

Cryptocurrency has always had a volatility problem.

Prices swing wildly. Fortunes appear and disappear overnight. It’s exciting – until you actually want to use it as money.

Because money isn’t just about growth. It’s about stability. Predictability. Trust.

That tension is exactly what led to the rise of stablecoins – a type of digital currency designed to hold a fixed price, often pegged 1:1 to the US dollar. In theory, one coin always equals one dollar. Simple.

In practice? Not always.

Behind that promise sits a mix of fiat reserves, crypto collateral, and, in some cases, fragile algorithmic models that don’t always hold up under pressure. And when they fail, they can fail fast.

What started as a niche workaround for traders navigating volatile cryptocurrencies has evolved into a multi-billion-dollar market – now sitting at the intersection of traditional banking, decentralised finance, and global payments.

So how did stablecoins go from scrappy experiment to financial infrastructure?

Let’s look at the history of stablecoins.

What are Stablecoins?

So, what exactly are stablecoins?

At their core, stablecoins are a type of digital currency designed to maintain price stability in an otherwise unpredictable market. Unlike most crypto assets, which are known for sharp swings in value, stablecoins aim to hold a stable value – typically pegged 1:1 to a stable asset like the US dollar.

This idea didn’t come out of nowhere.

Stablecoins emerged as a direct response to the chaos of cryptocurrencies, giving users a way to move through the crypto ecosystem without constantly being exposed to market fluctuations. Instead of converting back to fiat money through traditional bank transfers, users could stay within the crypto-sphere – holding a digital asset that preserved their purchasing power.

In other words, stablecoins became a kind of middle ground:

- Part digital money, built for speed and flexibility.

- Part fiat currency, designed for stability and everyday use.

And that balance is exactly what makes them so powerful.

Today, stablecoins play a central role in everything from crypto trades to cross-border transactions and international payments, allowing users to move value quickly across multiple exchanges without relying on traditional financial institutions.

But here’s where it gets more interesting (and more complicated).

Because while most stablecoins aim to maintain a stable value, the way they achieve that – and the level of risk involved – can vary dramatically. Some are backed by real-world reserve assets. Others rely on crypto collateral. And some depend entirely on market dynamics.

And as the history of stablecoins shows, not all of these approaches hold up under pressure.

So if the goal is always the same – stability – why are the outcomes so different?

It all comes down to how they’re built.

The Four Types of Stablecoins

Not all stablecoins are built the same – and that’s where things start to get interesting.

On the surface, they all aim to do the same thing: maintain a stable value and hold a fixed price. But behind the shared goal are very different pricing models, each with its own approach to price stability, risk, and reliability.

In fact, the history of stablecoins can almost be mapped through these designs – from early experiments to more sophisticated systems.

Broadly, most stablecoins fall into four categories:

Fiat-Backed Stablecoins

The most straightforward – and still the dominant force in the stablecoin market.

These are backed by traditional fiat currency like the US dollar, held in reserve assets such as cash or short-term treasury securities. For every coin issued, there’s supposed to be an equivalent amount held in reserve – making them ‘fully backed’.

This model is simple, familiar, and widely trusted, which is why fiat-backed stablecoins account for well-over 90% of the market today.

But they’re not without risk.

They rely on third parties – banks, custodians, and financial institutions – which introduces counterparty risk. If reserves aren’t properly managed or transparently reported, confidence can quickly erode.

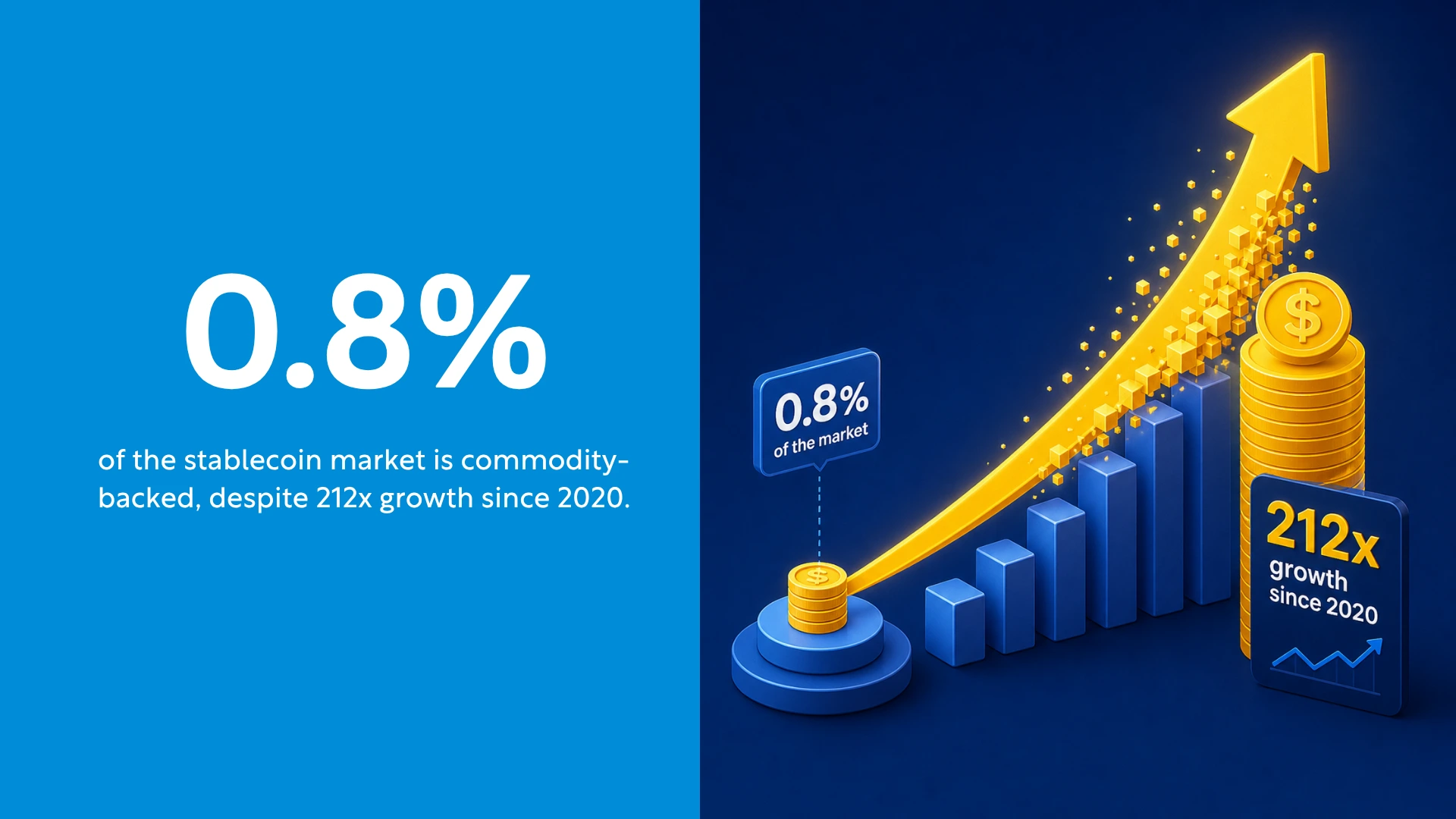

Commodity-Backed Stablecoins

Less common, but still part of the ecosystem.

Despite commodity-backed stablecoins rising by an astonishing 212x since 2020, they still account for just 0.8% of the market capitalisation – a tiny slice of the overall stablecoin market.

Instead of fiat money, these stablecoins are backed by physical assets like precious metals, most commonly gold. In theory, this ties their value to something tangible, offering a form of digital money that isn’t directly exposed to fluctuations in fiat currency.

They can appeal to users looking to hedge against currency substitution or diversify away from dollar-denominated assets. But despite their rapid growth, they remain a niche compared to the overwhelming dominance of fiat-backed stablecoins.

Cryptocurrency-Backed Stablecoins

A more crypto-native approach.

These stablecoins are backed by other crypto assets, often locked into smart contracts as crypto collateral. Because those underlying assets can be volatile, they’re usually overcollateralised – meaning more value is locked than is issued.

This model removes reliance on traditional banks and leans into decentralised finance, making it a core building block of DeFi protocols.

But again, there’s a trade-off.

If the value of the underlying collateral drops too quickly, it can trigger liquidations – putting pressure on the stablecoin’s ability to maintain its stablecoin peg.

Non-Collateralised (Algorithmic) Stablecoins

The most ambitious – and the most fragile.

Rather than being backed by reserve assets or collateral, these algorithmic stablecoins rely on code. Supply is automatically adjusted based on demand to maintain a stablecoin peg.

On paper, it’s an elegant solution – a fully decentralised way to create a stable value without relying on banks or traditional financial institutions.

But in reality, the model can be extremely fragile.

Without tangible backing, these stablecoins depend heavily on market confidence. And when that confidence starts to slip, the system can quickly unravel – triggering what’s known as a death spiral, where falling prices fuel panic, redemptions accelerate, and value collapses at speed.

History of Stablecoins Timeline

Stablecoins didn’t just appear fully formed – they evolved quickly, shaped by experimentation, explosive growth, and a few very public failures.

From early attempts to a stable digital currency, to a stablecoin market now worth hundreds of billions in market capitalisation, each milestone tells part of the story.

BitUSD (July 2014)

The story of stablecoins arguably begins with BitUSD – widely recognised as the first stablecoin.

Launched on the BitShares Network, BitUSD took a bold approach. Instead of relying on fiat currency held in a bank, it used a crypto-backed stablecoin model, locking up crypto collateral to maintain its stablecoin peg to the US dollar.

At the time, this was groundbreaking. It introduced the idea that price stability could be achieved without traditional financial institutions, using blockchain-based mechanisms instead.

But it also exposed an early flaw.

Because the system depended on the value of unstable cryptocurrencies, any significant drop in collateral could put pressure on the peg. And that’s exactly what happened – by 2018, BitUSD had effectively collapsed after failing to maintain its stable value.

Still, it proved something important: the idea of a stable, blockchain-based currency was possible – just not easy.

Tether/USDT (October 2014)

Just a few months later, everything changed with the launch of Tether.

Unlike BitUSD, Tether took a much simpler route: fiat-backed stability. Each USDT token was promised to be backed 1:1 by reserves, primarily consisting of cash and cash-equivalent assets, making it the first widely adopted fiat-based stablecoin.

That simplicity made it incredibly powerful.

At a time when much of the world still viewed cryptocurrency with scepticism – as speculative and disconnected from real-world use – Tether introduced something far more practical: a stable digital currency that could actually be used.

Suddenly, stablecoins weren’t just an experiment. They had a clear role.

Traders could move between crypto assets without cashing out into traditional bank accounts. Funds could flow seamlessly across multiple exchanges. And for the first time, there was a credible bridge between fiat money and the crypto ecosystem.

But that shift came with a new kind of tension. Because while Tether enabled real-world use cases – from crypto trades to early forms of cross-border transactions – it also introduced a fragile balancing act. Its price stability depended not just on design, but on trust in its reserve assets.

And that trust was repeatedly tested. Questions around transparency, audits, and the true backing of the USDT raised concerns – highlighting a core challenge that still defines the stablecoin market today:

How do you maintain a stable value in a system that still relies on confidence?

Tether didn’t solve that problem. But it proved that stablecoins weren’t just possible – they were necessary.

Dai (December 2017)

By 2017, the conversation had changed once again – this time towards decentralisation.

Enter MakerDAO and its stablecoin, DAI.

DAI refined the idea of cryptocurrency-backed stablecoin, using smart contracts and overcollateralised cryptocurrency assets to maintain its peg. No central issuer. No reliance on traditional banks. Just code.

This made it a foundational asset in decentralised finance (DeFi) – enabling lending, borrowing, and liquidity across the ecosystem.

But it also reinforced a key trade-off: Greater decentralisation often comes with increased complexity – and new forms of risk tied to collateral instability.

USDC (September 2018)

If Tether proved demand, USDC focused on trust.

Launched by Circle, USD Coin positioned itself as a more transparent, regulated alternative in the growing stablecoin market.

It doubled down on:

- Clearer reporting of reserve assets.

- Stronger alignment with emerging regulatory frameworks.

- Closer ties to traditional financial institutions.

This marked a significant evolution. Stablecoins were no longer just tools for crypto enthusiasts – they were beginning to align with traditional banking expectations and compliance standards.

TerraUSD/UST Collapse (May 2022)

Then came the moment that changed everything.

The collapse of TerraUSD in May 2022 sent shockwaves through the entire crypto market.

UST was an algorithmic stablecoin, designed to maintain its fixed price through a system of incentives rather than reserve assets. For a time, it worked quite well.

Until it didn’t.

As confidence dropped, redemptions surged. The system entered a death spiral, and within days, around $45 billion in market capitalisation was wiped out.

It was a brutal reminder that not all stablecoins are built to withstand stress – and that price stability can disappear faster than it’s created.

But it also triggered something else …

A global push for stronger customer protection and clearer regulatory frameworks.

Mainstream Integration (2023–2024): PayPal Launched Its PYUSD Stablecoin (2023)

After the chaos came consolidation – and a move toward legitimacy.

In 2023, PayPal entered the space with its own stablecoin, PYUSD, signalling a major shift toward mainstream adoption.

This wasn’t just a crypto-native evaluation anymore.

Stablecoins are now being positioned as tools for:

- International payments.

- Cross-border transactions.

- Day-to-day payments.

At the same time, regulators stepped in. Frameworks like the Europe’s Markets in Crypto-Assets Regulation began shaping how stablecoin issuers operate – focusing on reserve assets, transparency, and systemic risk.

Stablecoins were growing up.

Market Scale (October 2025)

By October 2025, the stablecoin market had reached a new milestone:

Over $300 billion in market capitalisation, with the market continuing to grow beyond that level.

And in the US, that shift became official.

The introduction of the GENIUS Act marked a pivotal moment – establishing the first federal regulatory framework for stablecoin issues, with a clear focus on consumer protection, reserve transparency, and ensuring stablecoins are backed by high-quality reserve assets.

It signalled something bigger than regulation alone:

Stablecoins weren’t just growing; they were recognised as part of the financial system.

What Comes Next for Stablecoins?

Stablecoins have already come a long way. What comes next will be defined by trust, regulation, and real-world use.

As financial institutions, central banks, and regulators step further into the space, the challenge will be maintaining price stability at scale – without losing the speed and flexibility that made stablecoins so powerful in the first place.

It’s a space that’s still evolving – fast.

And while the technology continues to mature, the brands behind it face a different challenge: how to stand out, build credibility, and communicate value.

That’s where deep industry understanding matters. With over 10 years in fintech and payments, we’ve seen these shifts play out time and time again – and we know how to turn complex topics like stablecoins into content that actually connects.

Because knowing where stablecoins are going is one thing. Knowing how to take them there is another.

If you’re building in the stablecoin space, you won’t need to over-explain it to us. Let’s talk.