- AI Visibility: How Brands Get Surfaced in Large Language Models - January 9, 2026

- Best Fintech Marketing Campaigns - November 3, 2025

- 5 Fintech Copywriting Tips That Actually Work - November 3, 2025

The movie Minority Report (2002) is set in the year 2054.

In it, eye scanners are so integral to everyday life, that the fugitive John Anderton (Tom Cruise) has to have his eyes replaced in filthy backstreet doctor’s room…

Biometric payments have long seemed like something related to a far-fetched future.

In recent years, there has been exponential growth in the use of biometric payment systems around the world.

Is it possible to securely purchase something online or in person, simply through the scan of a fingerprint? In this blog we’ll find out.

We’ll also explore exactly what biometric payment is and what it means for both consumers and merchants.

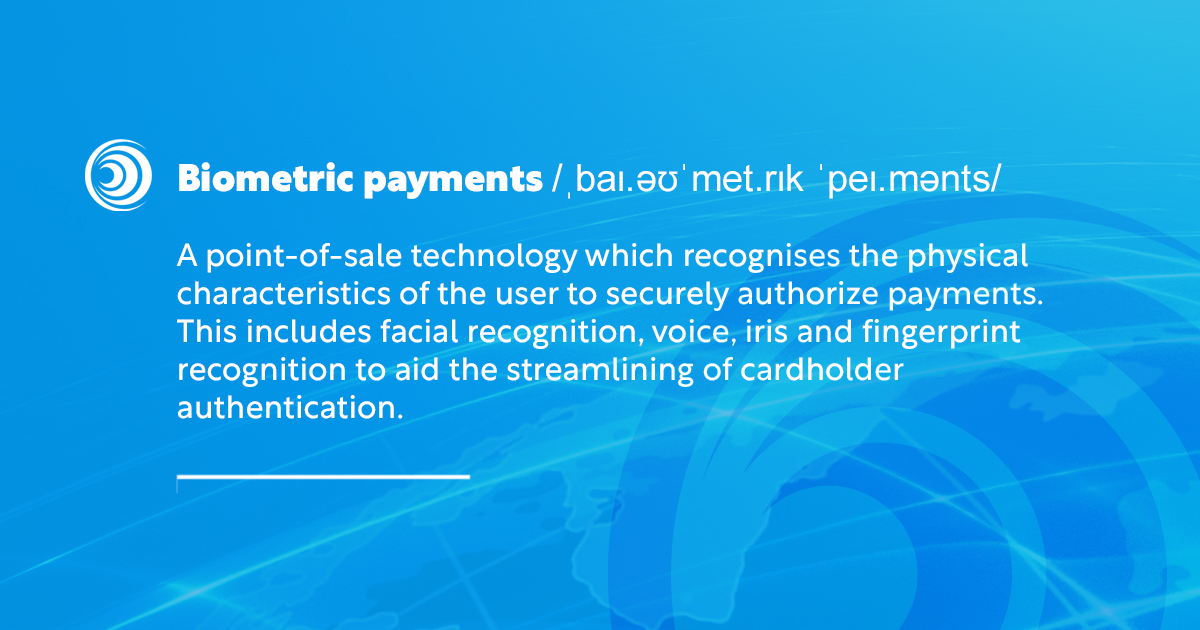

What is biometric payment?

Biometric payment is any point-of-sale (POS) technology that recognises physical characteristics of the user to securely authorise payments.

Facial recognition, voice, iris and fingerprint recognition aid the streamlining of cardholder authentication.

These biometric authentication methods aim to reduce friction when it comes to authenticating secure payments.

This usually applies to two-factor authentication, which requires two distinct forms of identification to verify a consumer’s identity to prevent fraud.

It is projected that between 2020 and 2025, contactless mobile transactions protected by biometrics will rise by over 520%, says StartMyLLC.

Where do biometrics fit in the evolution of payments?

Before civilisations appeared, people likely traded directly in goods.

Then cash began to appear independently in many societies. Coins appeared first, then the first paper money in Song dynasty (960 – 1279 AD) China.

Early forms of financial technology appeared in the 19th century, when money began to be sent electronically.

Then, in the late 20th and early 21st centuries, contactless payments really took off.

Mobile payments (a kind of contactless), accelerated this in the 2010s. And with mobiles, biometric authentication appeared for accessing phones, apps, and payment features.

How do biometric payments work?

Biometrics use the unique physical characteristics of the cardholder to authenticate a transaction.

Biometric payments use biometric data to corroborate a cardholder’s characteristics to authenticate payments.

Biometric payments are often seamless, although they may sometimes falsely identify a discrepancy in accordance with the biometric data.

This occurs if, for instance, the cardholder’s finger is wet when trying to make a payment.

Biometric cards

Consumers can be issued a biometric card by providing valid identification and bank account details.

When registering, the customer records their fingerprint with the issuer’s fingerprint scanner. The biometric data will then be encrypted and recorded in a centralized database.

At point-of-sale registers, the consumer can now opt for the biometric payment option with their biometric card and scan their fingerprint in addition to entering their PIN code.

If the biometric authentication is successful, the funds are transferred from the consumer’s bank account to the merchant.

Biometric payments can also be contactless, or made via mobile wallet.

In the event that the biometric payment card may be dropped or lost, fraud is made almost impossible. Other types of payment cards still face this risk.

In recent years, facial technology has also grown in use. For example, in Japan and Taiwan, 7-Eleven are looking to integrate it into their stores.

Fingerprint payments are currently the most widespread use of biometric technology.

Some stores in New Zealand have even been looking to implement facial recognition.

Example of a biometric credit card: Thales Gemalto

An example of a biometric payment card is the Thales Gemalto biometric credit card.

Based in Paris, France, the Thales Group are a multinational company that develops and manufactures electrical systems, devices and equipment.

Their biometric card combines a fingerprint sensor and EMV technology.

This means it meets the world standard for taking credit card transactions at physical point-of-sale locations and virtually.

Thales have already developed over 20 projects in the biometrics field. They believe fingerprint biometrics are set to be the authentication method of choice for EMV payment cards.

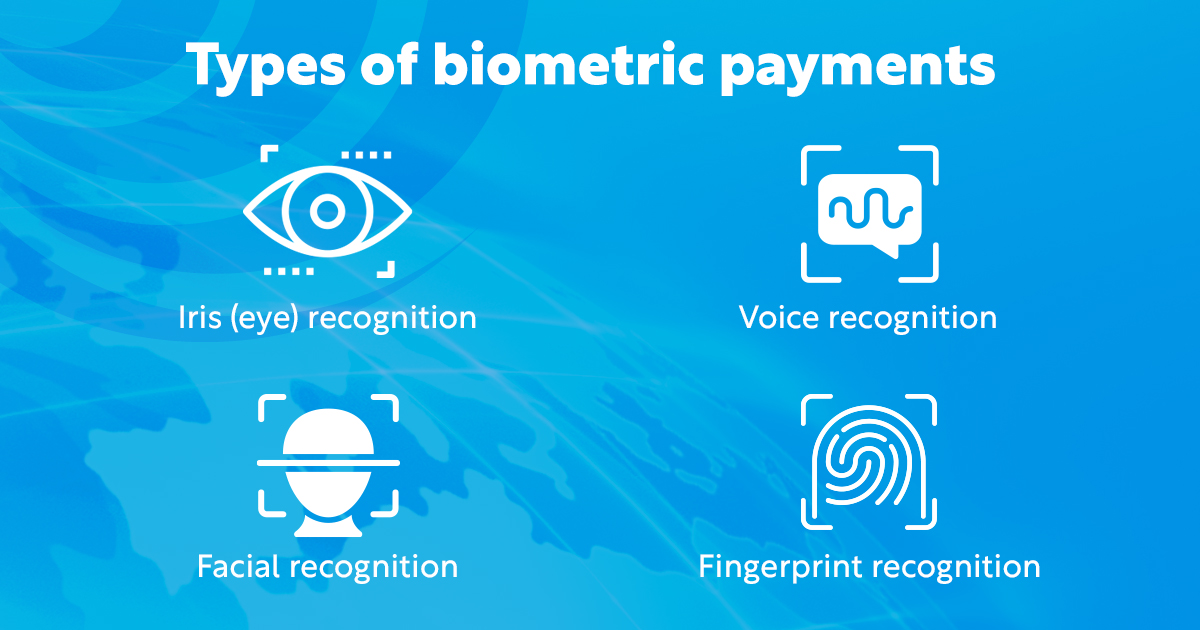

Types of biometric payments

1. Iris (eye) recognition

Iris scanning technology takes high-contrast photographs of a person’s iris using near-infrared light.

It is not a widely accessible form of biometric authentication because of its specialised equipment.

An example of this kind of biometric payment is PayEye. PayEye uses biometric iris scanning technology alongside a micro-banking system.

It takes a digitally scanned image of the iris which is then converted into special code for payment authentication.

In addition to authenticating payments, iris scanning is very useful to law enforcement officers.

They are able to match iris scans to images of suspects from an existing database in order to quickly and accurately confirm the suspect’s identity.

2. Voice recognition

Voice recognition technology identifies the characteristics of a consumer’s voice, then stores the biometric data in a database.

The audio input is then processed by software that is able to split the audio into multiple frequencies. Behavioural attributes are also identified that work in unison with the frequencies to build the voice print.

Biometric voice recognition provides a seamless payment experience for consumers. It eliminates the need for passcodes, PIN codes or additional questions intended to verify a user’s identity.

Voice data is can be used for authenticating biometric payments, granting access to particular devices or software.

Many mobile banking applications implement this biometric technology. Law enforcement may also use these audio prints in fraud detection investigations.

3. Facial recognition

Facial recognition is one of the most commonly used forms of biometric technology.

It is used by 14% of businesses according to StartMyLLC. Many new models of smartphone implement this feature to gain access to it.

A facial recognition algorithm processes the geometry of the person’s face from a photo, then identifies key distinguishable facial landmarks. It is then transferred into code known as faceprint.

The faceprint can then be compared to existing biometric data for verification.

Similar to biometric voice recognition, facial recognition allows for an input-free payment experience.

An example is the Apple Pay functionality of the later versions of the iPhone and iPad. It uses fingerprint and facial recognition software to authenticate payments on mobile devices.

Android phones have since followed suit, using facial recognition to verify purchases and unlock devices in Google’s Pixel 6 model.

4. Fingerprint recognition

Fingerprint scanners create a digital map of the customer’s fingerprint. If a person’s fingerprint corroborates with the existing data, they may bypass the password or PIN entering process.

Making a fingerprint payment streamlines the payment experience, albeit marginally less than biometrics that do not require any manual input at all, such as facial recognition.

Advantages of biometric payments

1. Secure payments

Biometric payments offer additional security to the transaction process. It is far harder to mimic users’ biological features than to memorize a PIN or passcode.

Data is thoroughly encrypted so in the event of a data leak the risk of fraud is lessened greatly.

Similarly, if a person were to attempt fraud, there would be record of their biological prints in the biometric system so they would be easily identifiable by law enforcement.

Facial recognition used in an FBI case

On August 10th 2018, the FBI had a search warrant against a 28-year-old man named Grant Michalski, a resident of Columbus, Ohio. They suspected he was in possession of child pornography.

The FBI told Michalski to place his face in front of his phone camera to unlock the Face ID mechanism so they could search his phone. The content of the phone eventually led to his arrest.

This case marks the first known case in which law enforcement used Apple ID facial recognition technology to open a suspect’s phone.

2. A faster payment process

There is no need for physical input when making a biometric payment. Users do not need to find, recall nor enter passwords in order to verify their identity.

Mobbeel says that transaction response time for consumers is reduced by around 80% with the use of biometric signatures.

3. No need to carry cash or cards

Biometric payments are very convenient. No cash nor payment card is necessary.

And when making a payment online, for example, the user does not need to find and enter their debit or credit card details either.

4. Lower costs for businesses

The cost per transaction for merchants using biometrics is lower than the cost per transaction when a debit or credit card is used. It is a far more economically viable option for businesses.

Disadvantages of biometric payments

1. Conspiracies

The association between fingerprint scanning and law enforcement sparks controversy among consumers. Sceptics fear that fingerprint sensors could be available to government agencies and officials.

Biometric payment services are quick to point out that only the fingerprints’ encrypted code is stored in databases, not the fingerprints themselves.

However, it does not escape the criticism that such payment systems are only as secure as their associated databases and transactions. No payment system is completely fool-proof.

2. Expensive to implement

Biometrics involve advanced technology that is expensive to implement. They are too expensive for most merchants to offer.

The cost of the hardware and software is very high. It could cost anywhere between thousands to millions of pounds to implement biometrics at checkout.

Aside from initial costs, merchants will need to purchase biometric data storage. Maintenance and customer service costs are also exceptionally high.

Conclusion

Biometric payment are increasingly popular. The market for them is predicted to rise by 520% in the next few years alone.

They offer better security comparative to other payment methods.

Their greatest selling point, however, is their ability to reduce friction in the payment process.

Constantly searching for payment details, passwords, PIN codes and the answers to verification questions can quickly become tiresome.

Users would be far less deterred from making payments with these obstacles removed.

Biometric solutions may very well lead the way to a cashless, card-less economy.